BCO/CoStar Office Outlook series: Key takeaways and trends for 2026 and beyond

Six city tour delivers unique insights into direction of office market for BCO members

Earlier this year the BCO teamed up with CoStar to tour the UK providing a unique and focused look at the UK office market, where it has been and where it is going. Over the course of three weeks, we visited six cities – London, Glasgow, Birmingham, Bristol, Manchester and Cambridge, and interacted with more than 400 BCO members.

Here, we share key takeaways and insights from all six presentations.

Executive summary

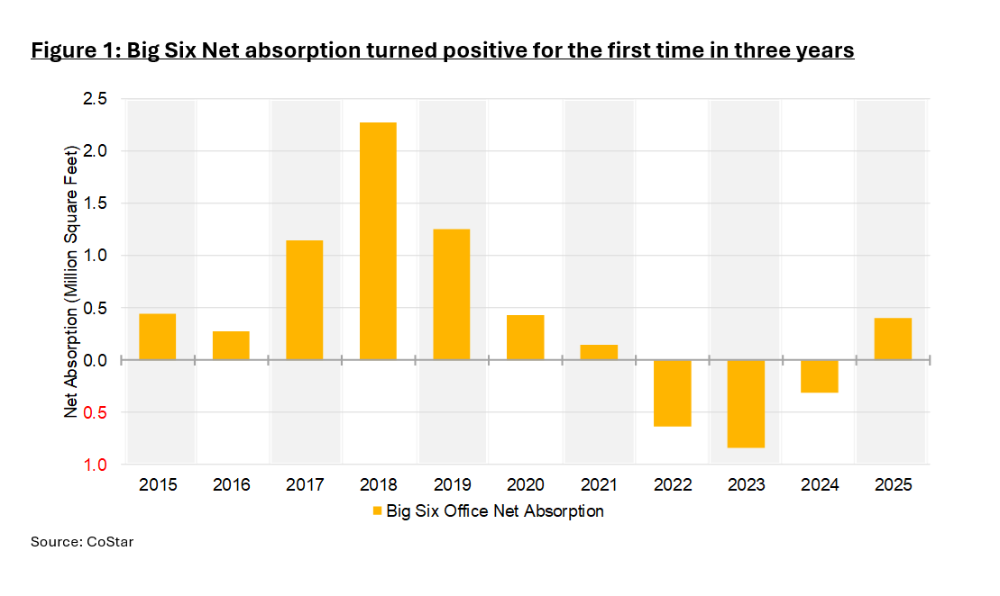

- Recovery, but uneven: Net absorption turned positive through 2025 (Figure 1) and vacancy has broadly stabilised, yet remains elevated in weaker sub markets; CBDs lead recovery while older/out of town stock lags.

- Two tier market is entrenched: Prime/new or best in class refurbished assets lease faster at rising headline rents; secondary stock faces persistent obsolescence pressure and, in places, conversion.

- Development drought supports rents: Starts are thin outside London; even in the capital a meaningful slice of pipeline is pre committed, pushing earlier campaigns and pre lets. retrofit-first is the default route to viability.

- Costs shape decisions: High fit out and build costs elongate leasing cycles and push demand toward fitted/managed product that de risks capex and speed to operate, while also meeting tenants’ growing preference for greater flexibility in lease terms.

- Amenity & experience are decisive: ESG is now “entry ticket”; location, cost, certainty, amenity and customer experience drive choices.

- Regions diversify the story: Bristol and Glasgow are supply constrained with rising rents; Manchester shows breadth of demand but 2026 new delivery is thin; Birmingham is opportunity rich but needs identity and amenity uplift; Cambridge is simultaneously over and under supplied as construction rises.

The national picture

The market has turned a corner. Leasing volumes and net absorption improved through 2025, stabilising vacancy. Normalisation will take time, however, as legacy space is re priced or repurposed. The “flight to quality” has hardened into a two tier market. Prime assets (including deep refurbs) are outperforming, while older peripheral stock trends to repositioning or change of use. Investment pricing mirrors this bifurcation.

Outside London, new starts are sparse; London’s pipeline to 2030 is partially pre let, effectively compressing uncommitted supply. High all in build costs tilt decisions toward retrofit-first where floorplates allow, with pre lets increasingly required for new build. Elevated shell/core and £300-£500 per sq ft – in London – fit out costs are a strategic constraint. Data centre/infrastructure demand is also pulling on contractor capacity – making deliverability a competitive edge.

With high build costs and limited contractor capacity, deep refurbs that decarbonise MEP, uplift EPC and other sustainability credentials, and add visible amenity will out compete speculative new builds unless exceptional site/floorplate economics apply.

The market is shifting to hospitality led offices: fitted/managed floors; club floors and outdoor space; credible wellness; high quality end of journey; and data led post occupation tuning. Target 3,000 to 5,000sq ft turnkey suites, 10,000 to 15,000 sq ft grow on, and 20,000+ sq ft whole floor options with pre marketed fit out standards.

In the investment market, liquidity is back for the very best assets, while regional opportunities skew to value add and refurb plays; forced sales and price discovery may create selective entry points. Overseas, especially US, buyers eye relative value in the UK regions as yields remain wider than London. Disposals from funds reaching maturity extensions may unlock opportunities.

The regional picture

- London & the South East

Capital flows rebounded in 2025, with large lot sizes clearing and prime yields tightening; Elizabeth Line continues to reshape occupier maths and footfall. Pipeline scarcity continues. Refurb-first often wins vs £1,000-£1,300 per sq ft new build costs. - Manchester

Demand breadth across TMT, education, professional/financial services; prime rents £45 per sq ft with £48-£50 in view. New delivery in 2026 is thin; >1m sq ft under construction skews to 2027–28. Flex enlarges to full floors. - Glasgow

While on first glance vacancy figures in the city look high, true Grade A vacancy sits at just 0.3% to 0.5%, with those headline vacancy figures overstated by unlettable stock. Rents are moving toward £50 per sq ft with selective £55-£60 per sq ft by 2030 for a small cohort. Funding is hampering new build, while rates relief changes weigh on heritage refurb capex. - Birmingham

Core markets (Colmore/Paradise) lead demand recovery; however, very thin Grade A supply and tough viability (yields, costs) make refurb the main lever. The city needs clearer identity/amenity to capture inward investment. - Bristol

Among the best performing regional markets; leasing at multi year highs. Severe Grade A shortage (only 126,000 sq ft available) implies pre let driven delivery and rent growth (trajectory to £55-£60 per sq ft by 2027). Demand for fitted, amenity rich space is pronounced. - Cambridge

A market of contradictions. Construction starts are on the up, temporarily lifting vacancy in some mid sizes. The long term fundamentals are strong, despite weakness in the life sciences market.

Outlook: What to expect in 2026 and beyond

- Rents: Prime headline rents continue to rise in supply starved cities (notably Bristol, Glasgow, selective West End sub markets); secondary rents diverge or flatten without capex.

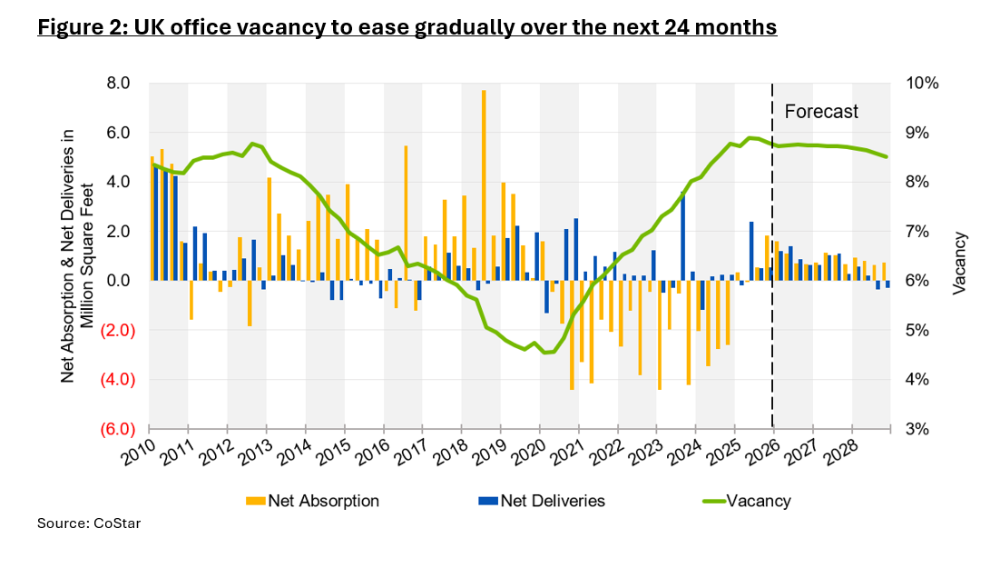

- Leasing: Earlier pre-lets; more best and final processes on scarce prime floors; greater use of fitted/managed for speed and capex certainty. Vacancy to remain stable over the next 24 months (Figure 2).

- Supply: A refurb led cycle dominates 2026-2028; new builds cluster later in the decade where pre lets and funding align.

- Repurposing: Out of town 80s/90s and weak secondary assets see heightened conversion and selective demolition where refurbishment is not viable.

10 key takeaways

1. Pipeline scarcity = pricing power for true prime; prepare for rent led viability and earlier pre lets, especially in London, Bristol, and Glasgow.

2. Retrofit first wins in most regional cases: faster delivery, lower embodied carbon, and lower risk than £1,000-£1,300 per sq ft new builds.

3. Experience is the tie breaker: service, programming and amenity beat certificate one upmanship when budgets are tight.

4. Cost certainty sells: fitted/managed floors at 10,000 to 20,000 sq ft help occupiers overcome capex/fit out barriers and speed moves.

5. Target real demand bands: persistent strength in 3,000 to 5,000 sq ft and 15,000 to 20,000 sq ft; 8,000 to 12,000 sq ft is harder.

6. Regions aren’t monolithic: Bristol = acute Grade A shortage; Glasgow = ultra tight true prime; Manchester = sectorally broad but 2026 delivery thin; Birmingham = identity/amenity challenge; Cambridge = temporary vacancy from rising construction.

7. Investment is back for the best; core capital is on the look-out, with selective value add via refurb and opportunistic entries expected as fund maturities unwind. In London, more big-ticket transactions are anticipated.

8. Delivery capacity is strategic: contractor scarcity (data centre drag) means early supply chain lock in and credible deliverability stories will win mandates.

9. Policy levers matter: targeted rates relief and planning performance agreements can unlock heritage refurb and election proof delivery timetables.

10. Talent is a planning issue: placemaking and city amenities (food, culture, active travel) directly affect occupancy and retention, councils and owners should act jointly.